Best in Five: EC&M's 2013 Top 50 Electrical Contractors Special Report

The electrical contracting industry’s upper echelon — those slotted on EC&M’s annual Top 50 Electrical Contractors list for 2013 — appeared to edge closer to “escape velocity” in 2012 from business-activity lows registered in the wake of the Great Recession. Whether that’s really been attained, though, is an open question, as the economy appears to still be walking a tightrope between modest growth and retrenchment.

But as a group, this year’s Top 50 firms (to see a copy of the Top 50 Electrical Contractors List in PDF form, click here), ranked by 2012 revenues reported via the annual proprietary EC&M survey, racked up 9.4% more for the year over 2011. Collectively, the leading companies generated $14 billion in revenue — up from the $12.8 billion reported by 2012’s Top 50 firms.

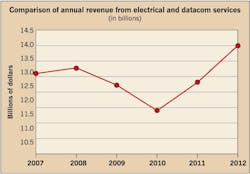

Inflation notwithstanding, that raw revenue number is the Top 50’s highest in at least the last five years — going back to 2007 when revenue came in at just over $13.1 billion. The low point in that span was 2010, when collective revenues were clocked at $11.9 billion, and the industry was still regaining its footing (Fig. 1).

That 17.6% swing from recent trough to the new 2012 peak likely reflects growth tied to the broad, but still shallow, economic rebound as well as the rebirth of projects that were mothballed during the financial crisis. But there’s also evidence that it ties to the steady escalation of demand for services in sectors that are experiencing outsized growth in an evolving economy, such as energy, information technology, and health care, as well as contractor efforts to insert themselves into areas that can yield new sources of project-related revenue and improved margins.

Anecdotal evidence from some Top 50 respondents suggests the 2012 revenue surge may be largely due to the unleashing of pent-up demand and the clearing of backlog.

Duane Hendricks, executive vice president of 35th-ranked Egan Company, Brooklyn Park, Minn., says the company’s 50% growth came from increased spending in areas that seem to be rebounding or drawing more funding. Infrastructure, manufacturing, education, and health care were all strong for the company.

“Transportation in our area is an expanding market, as more light rail and roadway projects take shape,” Hendricks says. “And manufacturing was good for us because we have a strong industrial controls group.”

M.C. Dean, Inc., Dulles, Va., No. 5 on the Top 50 list, experienced a 15% revenue falloff; however, it also saw signs that the market for electrical services was both firming up and evolving.

“Infrastructure opportunities look solid as well as sustainment,” says Sharon Hawkins, marketing and communications director. “We think a backlog shift into 2013 — delays in project starts and schedules — has largely concluded. We have an emerging renewable energy business that is still small, but emerging, especially on the design side.”

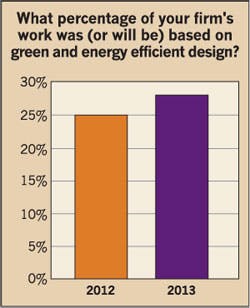

The latter may reflect a growing trend. A survey of the Top 50 found that, on average, 28% of a typical contractor’s work is based on “green and energy-efficient design,” as shown in Fig. 2.

Other companies in the Top 50 saw revenue growth from sectors where the stars are in near perfect alignment.

MMR Group (No. 4), Baton Rouge, La., for example, rode the surging domestic oil and gas boom to a Top 50-leading 132% growth in revenues, producing a top line good enough for fourth place on this year’s list — a spot that’s up from 10th place in 2012. Already entrenched in the energy business owing to its geographic location and an emphasis on process industrial electrical work and plant instrumentation contractor alliances, the company simply secured more work in 2012 as upstream, midstream, and downstream energy projects all flourished amidst favorable pricing structures.

“The fracking (hydraulic fracturing) boom, in states such as Colorado and Texas, has produced a good number of smaller projects for us, and we’ve also put 1,900 people to work in Canadian oil-sands projects, such as Imperial Oil’s Kearl venture there,” says Grady Saucier, vice president of marketing. “But there’s no one thing we can point to for our growth; mostly it’s the result of good planning and scheduling — and going where the work is.”

Just as MMR parlayed its location on the energy-intensive Gulf Coast into more business in the emerging energy economy, San Jose, Calif.-based Rosendin Electric, Inc. (No. 3), took advantage of its proximity to Silicon Valley to ratchet up revenue from business in the technology sector. The company, which boosted 2012 revenue 9% but slipped from second to third place in the rankings, continued to benefit from a proliferation of data center development work and massive campus and manufacturing buildouts by technology industry heavyweights.

“Data centers have been a big contributor to our growth the last few years, and it’s now to the point where they account for 10% of our business,” says Larry Hollis, vice president of marketing and development. “That’s really booming — going gangbusters — as is work in states like Arizona and Oregon on chip fabrication plants. Rosendin has developed a core group of people here who work with both end-users and general contractors in these areas.”

But even leading electrical contractors without an established or natural link to the technology economy seem to be landing more business in that rapidly growing corner of the market. In fact, according to Top 50 survey findings, respondents listed the “data center/mission critical” market sector second only to “health care” as the top source of dollar volume in 2012 (Table 1). By contrast, in the 2012 survey, data centers ranked fifth on the list of top dollar volume sources for 2011. With the exception of “education/institution,” the list of projected top market sectors for 2013 looks a lot like that for 2012. Health care again tops the list, followed by data centers, power, and private office (Table 2).

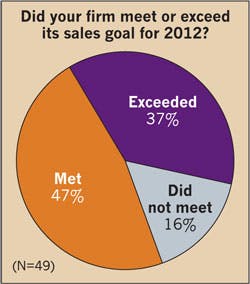

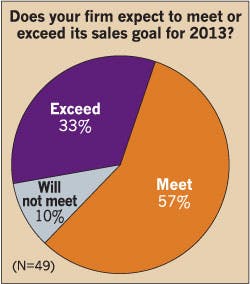

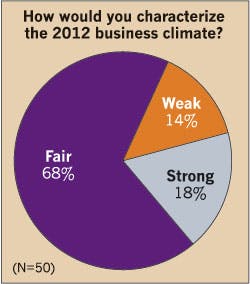

Whatever their individual sources of projected 2013 revenue, the Top 50 contractors are generally sanguine about their prospects for the current year. With the industry evidently reversing three consecutive years of slipping revenues in 2012, a solid majority of electrical industry leaders say midway through 2013 that their performance is falling in line with projections. Most — a full 57% — were optimistic they’d hit their revenue mark, while another 33% actually anticipated doing more business than they planned for at the outset of the year (Fig. 3). Tempered or not by fears of overconfidence or an economic-recovery head fake, those projections suggest a level of optimism that has probably been in short supply and which may yet prove unwarranted. After largely hitting or topping their 2012 sales goals — 47% of respondents indicating that they hit their target; 37% saying they exceeded it (Fig. 4) — the Top 50 includes just a handful of companies that report a possibility of not hitting their revenue mark this year. That’s a pretty optimistic outlook, considering the fact that nearly 70% of respondents characterized last year’s business climate as “fair,” as shown in Fig. 5, and in spite of a reluctance to say that the construction economy — still their lifeblood — is on the verge of a breakout.

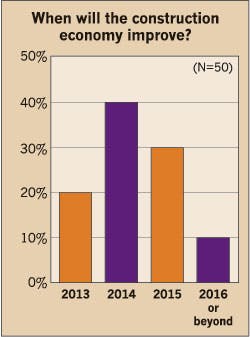

While the general economy may be showing relative improvement, a clear majority of Top 50 companies opine that the construction climate won’t show marked improvement for at least another two years. Eighty-percent of respondents said a recovery won’t be in evidence this year; to the contrary, 40% said it will come in 2014; 30% said it will be more like 2015; and 10% fear it’s 2016 or later (Fig. 6). It’s no surprise then, that when asked to attach a number to their 2013 expectations, responses are all over the board. Balancing the evident predictions of a slow return to normalcy in the construction market coupled with the reality that many companies’ revenues can experience wide year-to-year swings (even as long-term, up-or-down trends take shape), industry leaders are almost evenly split on their guidance for changes in revenue from 2012 to 2013.

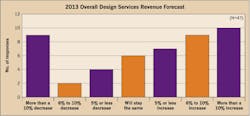

Almost 40% of Top 50 companies land at the two far ends of the spectrum on their revenue forecasts (Fig. 7). Nine said they’d see at least a 10% decrease in revenues, while 10 said they’re expecting an increase of more than 10%. But overall, more are anticipating at some least some increase — 26 compared to 15 companies eyeing a decrease. Just six are anticipating business to remain flat — testimony, perhaps, to the old saying that, in business, “you’re either growing or you’re dying.”

But there’s little evidence, in spite of a still-challenging business climate and pockets of underperformance and unrealized potential, that any of the Top 50 companies are mired in big slumps. While about one-fifth of the companies on the 2012 list did drop off, replaced by those new or returning, only about one-third reported revenue declines; the rest reported increases, many quite hefty, reflective of the group’s overall performance improvement.

One of the biggest movers among this year’s Top 50 was Ludvik Electric Co., Lakewood, Colo., which boosted its revenues 69% in 2012, taking it from No. 46 on the 2012 list to No. 33 this year. Indicative of the industry’s cyclicality, the 2012 performance followed a 2011 showing that produced only a fractional revenue gain from the prior year.

Richard Giles, company chief financial officer/treasurer, characterizes the big swing partly as the price an established Top 50 company pays for largely sticking to its strengths and not chasing hot market sectors. Although it has edged more into the emerging data center market — where one big project reaching its zenith was a big contributor to Ludvik’s revenue spike — it hasn’t pursued the growing multi-family market, which has been white hot in its own backyard.

“There are a lot of apartments going up in the Denver area, but that work isn’t a fit for us, so we can’t participate,” Giles says. “You need to be out there bidding and letting people know you’re alive, but our concentration is commercial/industrial. We’re not at a stage as a company where we’re doing things for practice anymore.”

The company has ridden the roller coaster the last several years, partly the result of wide swings in backlog, and it expects 2013 results to contribute to that trend. Ludvik now doesn’t expect to meet its revenue expectations for the year and sees the likelihood of a revenue falloff of more than 10% and possibly a need to trim its workforce. Data centers and water/wastewater markets will again be its top two revenue sources, but the power market could supplant public buildings as the third biggest source. Ultimately, though, the up-and-down revenue cycles don’t worry Giles because they come with the territory.

“You can’t look at this business month-to-month or even year-to-year, but rather on a much longer-term basis,” he says. “The real key to success is how you manage the projects you get and fine-tune the resources you have at your disposal.”

Being more nimble and opportunistic, too, can pay dividends, as Long Island City, N.Y., contractor, E-J Electric Installation Co., has demonstrated. The company, which moved up to the No. 13 spot from No. 20 in 2012 and No. 26 in 2011, last year secured large chunks of work repairing damage caused by devastating Hurricane Sandy. That work, largely for electric utilities and hospitals impacted by the storm, accounted for one-third to one-half of the 51% revenue gain the company recorded in 2012, says company chairman, J. Robert Mann, Jr. While that amounts to a one-time boost that will play out for another six months or so, that work did spur the company to position itself to expand its activity in the power sector. That’s where it sees emerging opportunities tied to the grim, but nonetheless real, prospect of more natural disasters and a steady push to improve national infrastructure. Mann projects that area replacing “sports/recreation” this year as a top market along with health care and transportation.

“There’s a niche to exploit there, so we’ve established a new power transmission and distribution line of business that will focus on post-disaster work, installation, and maintenance,” he says. “This is something that needs the kind of expertise we’ve developed.”

Meanwhile, E-J continues to ply its expertise in transportation, including work on protracted New York City subway projects, as well as power plant, substation, and high-voltage transmission-line projects. It’s also rounding out the mix with one-time negotiated projects, such as a large water treatment plant in the Bronx. Taken as a whole, E-J’s 2013 business is seen on track to meet pared-down expectations of a 6% to 10% slide in revenues, partly due to the expiration of Sandy-related work.

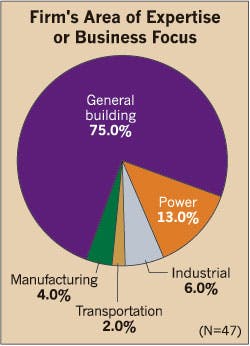

Niches are an important vehicle for boosting performance, but most top electrical contractors seem to be content with the “generalist” label (Fig. 8). Three-quarters of the Top 50 characterized their area of expertise/business focus as “general building,” encompassing commercial, institutional, health care, and housing work. The only specific area to get a double-digit percentage ranking was “power,” with 13%.

Finding the right mix of work that plays to strengths, offers respectable margins, and positions the business for the future is important, but leading companies also are focusing more on project internals as they evaluate prospective work. Projects structured in ways that present opportunities for subcontractors to be more involved in the early stages of planning and design offer an attractive balance of risk and reward and allow them to collaborate more closely with other trades to control costs and boost efficiency are emerging as key variables. It’s not surprising then that leading electrical contractors as a group seem to continue warming to the idea of exploring non-traditional methods of project delivery.

Two types — construction management at risk and performance-based design-build — gained in popularity last year, according respondents. On a list of eight delivery types, headed once again by more traditional design-bid-build and design-assist, construction management at risk rose from seventh to fifth place, while performance-based design-build advanced from fourth to third (Table 3).

Such approaches, notably BIM, are complementing design-assist and design-bid-build at Faith Technologies, Inc., a Menasha, Wis., contractor. Although it boosted revenue by a modest 5%, the company, again No. 17 on the list, is on track to increase revenues by at least 20% this year and could see another 20% in 2014, says Tom Clark, executive vice president of pre-construction. That optimism, he explains, stems partly from the company’s growing focus on honing expertise and selling competency in being a construction partner, not just a low bidder.

Faith used the economic downturn to develop an in-house pre-construction group oriented to bringing the company’s expertise in virtual and conceptual estimating, design, budgeting, and pre-fabrication to bear early in the project-formulation process. Health care, one of the company’s top markets, happens to be a good fit for such alternative project delivery concepts, so more business could be captured in that market, Clark says.

“Ultimately what you’re doing is providing them with a budget for what they’re trying to do, and then at the hiring stage all of the subs can be brought on board early and work together to build the project more efficiently and effectively,” he explains. “Hospital expansion and renovation work lends itself to early involvement, design solutions, and virtual estimating.”

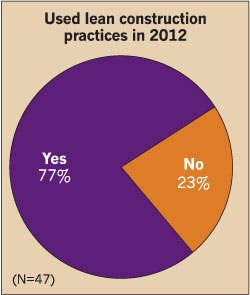

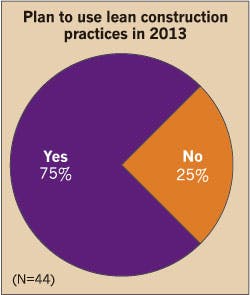

A vital component of many emerging project delivery methods — lean construction practices — continue to attract the interest of electrical contractors. With project profitability increasingly dependent on the ability to accurately forecast and control all costs, reduce waste, schedule properly, and align well with other trades, it’s understandable that lean construction looks to be at least an entrenched concept at a majority of top contracting firms. More than three-quarters of survey respondents said they used lean construction practices in 2012 (Fig. 9) and nearly the same number plan to again in 2013 (Fig. 10). That’s up from about two-thirds of last year’s respondents.

Lean construction is a natural complement to Faith Technologies’ emerging emphasis on project efficiency, Clark says. It’s so central that the company has created a “Faith Performance Advantage” initiative broadly focused on maximizing job-site productivity. One tenet is the “30-30 rule” that aims to put everything a worker needs on a job site within 30 feet or 30 seconds of where they’re working. Another “best practice” is the use of two-way radios that allow ready communication between the superintendent, foremen, and leads. The simple aim, he says, is improved productivity that

ultimately shows up on the bottom line. But for all of its common sense practicality, lean construction probably remains a work in progress for many contractors. M.C. Dean, Inc., is now seeing some payoff when conditions allow for its use, as was the case with a recent hospital and data center project, says marketing director Hawkins.

“It’s starting to help,” she says. “It is very complex and requires a great deal of skill in design, modeling, fabrication, and sequencing of work. If the GC, mechanical, design, and owner are all committed, it can yield spectacular results.”

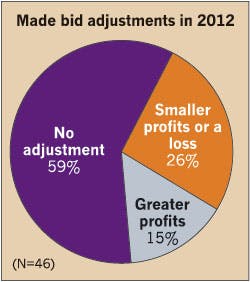

One such result, presumably, is higher job profits. But on that score, contractors, though seemingly eager to test the waters, appear resigned to the reality that the business climate won’t yet allow them to reach for higher margins. Fifty-nine percent of this year’s Top 50 said they didn’t make bid adjustments last year, while 26% said they adjusted their bids for smaller profits or a loss and 15% adjusted for greater profits (Fig. 11).

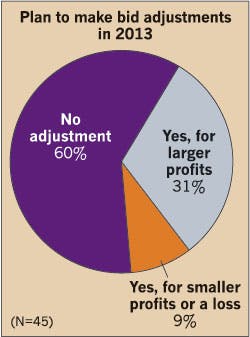

But in another sign that things may be firming up, 46% of last year’s Top 50 said they had adjusted bids for smaller profits or a loss in 2011, nearly double the 2012 number. But on the whole, contractors apparently aren’t letting that change their approach to bidding tactics for 2013. Mirroring last year’s survey, 60% said they were not anticipating bid adjustments, 31% said their bids would reflect a higher margin, and 9% suggested they’d probably have to sacrifice some profit to keep busy (Fig. 12).

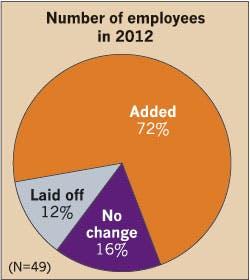

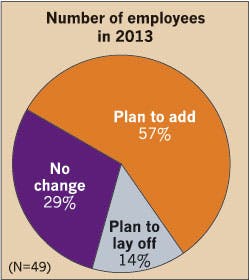

The steadiness of labor costs, a big wild card in profitability, has helped support contractor profits overall. But contractors also look to be in a hiring mode as more work beckons. Nearly three-quarters of the Top 50 respondents said they added employees in 2012 (Fig. 13), and 57% indicated they’d do so in 2013 (Fig. 14).

Improved productivity and labor management has helped brighten the profit picture, but with cutthroat bidding still evident, contractors are exploring other avenues to improve the bottom line. They include forging closer relationships with clients that can lead to more negotiated work and selling design and other pre-construction services that can amount to value-added propositions clients are willing to pay for.

At Power Design, Inc., St. Petersburg, Fla., which ranks No. 32 on the list, there’s a growing recognition that consistently profitable work results from careful project planning and the ability to get paid for bringing some insight and new thinking to the table. The company is strong in the multi-family construction arena and has ratcheted up data center work to account for 15% of its revenues. Profitability in those markets increasingly rests on careful project selection, intimacy with other parties, and clear expertise.“In the data center area, we’re fortunate to have a couple of good clients who we’re able to negotiate everything with, and in the residential market we have a lot of influence with developers on GC selection, which gives us some leverage,” says Lauren Permuy, vice president of business development.

But as the recent performance of the industry’s largest company suggests, profits for the industry as a whole don’t look to be in a break-out mode. EMCOR Group, Inc., Norwalk, Conn., the clear No. 1 leader on the Top 50 again this year, revealed that its operating income for the second quarter of this year was $51.3 million, down 10% from $57.1 million generated in the second quarter 2012. That number was also down as a percentage of revenue — from 3.7% in 2012 to 3.3% in 2013. Nevertheless, the company’s president and CEO, Tony Guzzi, struck a mostly positive note on the long-term outlook for revenues and profits in discussing EMCOR’s second-quarter numbers. Recent divestitures and reorganization, he says in a company press release, position the company to “succeed over the long term with improved profitability and growth prospects.” And EMCOR’s long-term focus, he says, is on “areas that we can control, including prudent cost discipline, opportunistic contract bidding, and investing in growth.”

That’s just one CEO talking, but it might well constitute the general roadmap for others on the Top 50 as they continue to chart a way out of the woods of a largely unprecedented, unforeseen, and prolonged slump.

Zind is a freelance writer based in Lee’s Summit, Mo. He can be reached at [email protected].

About the Author

Tom Zind

Freelance Writer

Zind is a freelance writer based in Lee’s Summit, Mo. He can be reached at [email protected].