It’s been five years since the financial crisis and crippling recession froze new construction in its tracks. Today, the U.S. economy continues to mend in a patchwork fashion, producing confidence that a slow and steady rebound in construction activity three years in the making can be sustained into 2014.

The consensus among industry analysts is that total construction growth in 2014 will again be modest, but possibly more evenly distributed than in past years. Forecasts generally see percentage growth in total construction square footage and spending at year-end 2014 landing in the mid- to high-single digits, a healthy pickup from the rate expected for 2013. With a few exceptions, growth is seen in the broad residential and non-residential sectors alike, as momentum that began to build in 2012 and 2013 carries over into the new year.

Still, forecasters don’t seem to know quite what to make of the big economic picture and the sustainability of construction’s bounce off of 2009 lows, which began in earnest in 2012. The economy, they caution, may still be saddled with fundamental problems and minefields. There could be chronic impediments to a return to normal and sustainable growth patterns. Stubborn unemployment, the specter of higher interest rates, unresolved battles over fiscal policy, and the prospect of an extended period of subdued GDP growth continue to cast a long shadow.

But amidst the uncertainties, there’s no arguing that recovery has occurred. For now, it’s perhaps enough that there’s a growing need and healthy appetite for more physical structures of all types that might even prove resilient to fresh economic headwinds.

“It’s a good news, bad news scenario,” says Randy Giggard, managing director of the Research Service Group of FMI Group, Inc., which publishes an annual U.S. Markets Construction Overview. “From where we are now, we’re seeing a mix of conflicting drivers impacting the market. The good news is that we’re seeing continued steady improvement in construction volume and backlogs that will likely accelerate. The bad is that there’s still a lot of uncertainty out there that makes people nervous. But sentiment seems to be slowly improving, and a slow recovery might really be a good thing.”

Robert Murray, VP of economic affairs for McGraw Hill Construction, which publishes the annual Dodge Construction Outlook (Dodge), says that on balance, the economic backdrop looks healthy enough to support at least another year of “measured expansion” of the construction market. Noting the challenge of “forecasting uncertainty,” which he said still abounds, Murray says respectable growth in 2014 is probable but still reliant on the continued stability of trends that have fed the recovery.

“The way things are shaping up is that this is going to be another step along the road to recovery, but it’s going to be

painful and frustrating at times,” Murray said in his presentation at the McGraw-Hill 2013 Outlook Executive Conference in October. “I think we all know that this is going to be a slow process.”

A growth phase

But it’s undeniable that construction has found its footing in the last several years — and that final numbers are almost certain to show that the trend continued in 2013. Dodge estimates that construction starts last year will come in at $508 billion, a 5% increase over 2012. That number looks more than two times better, though, taking out electric utility starts, which plummeted 55%. FMI checks in with a similar view of 2013 gains, valuing construction-put-in-place (CPIP) in 2013 at $910 billion, up 6%.

Looking just at the non-residential construction market, the AIA Consensus Forecast that crunches estimates from six forecasting entities put the 2013 number 2.3% ahead of 2012’s figure of $299 billion. Within that group, Associated Builders and Contractors (ABC) came in with the highest estimate — 4.7% — followed by FMI with 4.1%. But low side numbers were as low as a 1% decline.

Many of those forecasts are even more bullish for 2014. The AIA Consensus, for instance, is for 7.6% growth in non-residential construction, more than triple the predicted year-over-year growth rate for 2013. ABC is in the same ballpark, projecting a 7% gain, the same as FMI, which sees CPIP totaling $977 billion. Dodge sees total U.S. construction starts rising 9% to $555 billion, almost twice the growth rate that produced its $508 billion estimate for 2013 (see Fig. 1). Portland Cement Association in its Market Intelligence Outlook looks for an 8% boost in CPIP, a big jump over the 1.3% increase in 2013.

“Next year is shaping up to be pretty decent as there’s a fair amount of pent-up demand for various forms of construction and also a fair number of tailwinds that will push the economy forward, such as continued low interest rates, lower gas prices, and a booming stock market,” says Anirban Basu, ABC’s chief economist.

Market fundamentals for major construction sectors are “generally positive” and seem to point to further growth in 2014, says AIA’s Chief Economist Kermit Baker. A key barometer for him is the AIA Architecture Billings Index, which looks at trends in design activity. Baker says it has been staying above a key level that has historically signaled an upturn (see Fig. 2).

“Design activity is highly correlated with construction activity, leading it by nine to 12 months,” Baker said in his presentation for Reed Construction Data’s October webinar, 2014 Outlook: Emerging Opportunities for Construction. “We’ve seen scores above the important ‘50’ mark for 12 of the last 13 months, so we think it points to a sustainable recovery in non-residential design activity.”

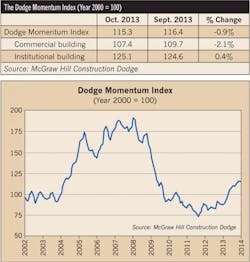

Another closely followed barometer, McGraw Hill’s Dodge Momentum Index that purports to forecast non-residential spending a year out based on initial reports for projects in planning, continues to climb. It has advanced 26% since December 2012 and has been rising at a rate last seen in 2004 (Fig. 3). However, it slid 1% in October, and the commercial building component gave back 2%.

The AIA index tracking commercial and industrial design activity has lately been turning up at the fastest rate of any sector. Baker says that trend may be significant.

“The residential activity index has been the strongest, largely fueled by a steep upturn in multi-family activity and the strong resurgence of single-family over the last 18 months, and a healthy home-improvement market,” he said. “The commercial/industrial sector has been unusually volatile in recent years, but in recent months that’s where we’ve seen the strongest growth, so it looks like that’s about ready to see some stronger construction activity moving forward.”

That’s suggestive of a broadening out of construction growth across different sectors, a measure that’s being closely watched as the construction recovery matures. It’s one that holds clues to the economy’s overall health as well as confidence that a sustained spending resurgence isn’t a mirage created by spikes in isolated sectors or off of deep lows. And it’s especially important at this point in the cycle. So much of the growth in construction over the last few years has come from the rebound in single- and multi-family home construction that it can obscure the true picture.

But signals are mixed as to whether construction growth will indeed be broad-based looking to 2014 and beyond. Comparing the various forecasts, one takeaway is that 2014 will likely see a cooling in some sectors that have had a hot hand in the last couple of years and a surge in those that have lagged. Another might be that it’s simply one step forward and two steps back in some markets. Yet another is that an important inflection point may be at hand in the demand for certain types of construction.

Housing marches on

Single-family housing, one of the stars of the last few years and a “canary in the coal mine” for the health of the economy and construction overall due to its link to consumer spending, will forge ahead in 2014, forecasts suggest. After a run-up that began slowly in 2010, slipped a bit in 2011, and began surging at a 25% to 30% clip through 2013, single-family housing starts are likely to keep accelerating in 2014.

Dodge sees the market growing by 26% in dollars, and 24% in units, to 785,000, in line with the expected 2013 gain. The National Association of Home Builders (NAHB) forecast sees 826,000 units being built in 2014, up 31% from the 629,000 units built in 2013, and the 17% gain it logged over 2012. FMI is less bullish, forecasting new-home construction value to be up 17% on the year.

Meanwhile, multi-family residential construction seems headed for a tapering of its torrid growth pace of the last few years. The sector has been booming as the fallout from the 2008 collapse of the single-family market sent more people to the rental market. Construction of apartments and other such dwellings took off, fueled by surging demand, low interest rates, and a supply shortage. Now, with that market becoming more saturated as vacancy rates level off, demand and construction is cooling.

In Dodge’s estimation, the pace of multi-family construction will continue to slow in 2014, but spending will still rise 11% to $53 billion, and total units built will increase 9%. The estimated 2013 figure of $48 billion would be a 19% gain over 2012. FMI also sees the sector tapering to 25% growth from 36%, and NAHB projects units-built to grow 10% to 326,000, a slowdown from 20% growth and 296,000 units in 2013.

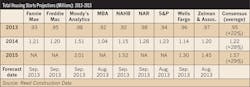

On balance, housing construction looks to be strong again in 2014 (Fig. 4), benefitting from a convergence of factors that add up to demand continuing to outpace supply. Despite the slow and still-choppy economic recovery, more movement is apparent in the housing market. Single-family home prices, rental rates, mortgage rates, and employment numbers are hovering around levels that could invite a flurry of action on the part of more buyers and sellers; there’s an uptick of interest in “household formation” on the part of formerly displaced homeowners; and borrowing costs for builders remain historically low.

With a forecast of 924,000 total housing starts in 2014, an 8% increase, NAHB sees the sector as still having a head of steam to carry it through 2015. In spite of ample challenges and risks that could mar the upbeat forecast, the group’s chief economist says housing should continue to pull its weight and more in the economic recovery.

“The cards are in play for a decent and fairly strong recovery in 2014 and particularly in 2015,” said David Crowe, speaking at the NAHB Fall 2013 Construction Forecast Webinar. “From the standpoint of GDP growth, housing has been a plus, growing at two, three, and four times the rate of the rest of the economy in recent quarters.”

Despite the long run-up in housing construction, FMI sees respectable, if not spectacular, growth for the sector, with CPIP hitting $380 billion in 2014. “Even though there has been some backpedaling, growth in residential continues to show some traction,” reads the executive summary of the FMI overview. “However, we expect the rapid growth to taper off to 12% in 2014.”

Stragglers join non-residential push

The pace of a long pickup in non-residential construction spending, meanwhile, is expected to stay restrained but respectable in 2014 (see Fig. 5). It could be aided by new signs of life in some long-dormant sub-sectors and despite fresh pullbacks in others that have followed a jagged course in recent years. Somewhat at the mercy of what transpires in the much larger residential sector — reflective as that is of the plight of the all-important consumer in this economy — the non-residential sector overall is seen tracking the broader economic recovery. As long as that continues, demand for new commercial, institutional, and manufacturing buildings is likely to follow suit.

“We’re seeing an emerging recovery in non-residential building activity, but it has been quite modest to date given how far it fell during the downturn,” said AIA’s Baker in the October Reed webinar. “On the non-residential front, there continue to be a broad range of uncertainties, financing issues and supply constraints are on the downside, and energy costs are on the upside, to mention a few that are out there.”

While heartened by the AIA Architecture Billings Index pointing to a likely pickup in some non-residential sectors, Baker illustrated the sector’s tepid performance of late with recent U.S. Census Bureau numbers. Construction-put-in-place in commercial/industrial and institutional fell 2.1% to $352 billion in the year ended last July. Institutional was the big drag, down 5%, but commercial/industrial was up 2.4%, led by the lodging sector’s 30% advance.

Within the AIA Consensus Construction Forecast for non-residential construction for 2013-2014, the six component forecasts ranged from a projected gain of 2.3% up to 9.7% for 2014, notably higher in most cases than the percentage gains they foresaw at mid-year for 2013. Overall, the AIA forecasts’ 7.6% growth prediction computes to some $350 billion worth of new non-residential construction in 2014.

The Dodge Outlook forecasts slower growth in non-residential construction starts. A non-residential market defined as commercial, institutional, and manufacturing buildings, as well as public works and electric utility projects, is seen reaching $302 billion in 2014, up fractionally from $300 billion in 2013 but well down from $320 billion in 2012.

Ken Simonson, chief economist for Associated General Contractors of America, sees a slightly better year on tap for private non-residential in particular, a continuation of its bumpy ride of the last several years.

“Private non-residential had a huge spike in January 2012, up more than 25% from a year earlier, but has since cooled and been growing at just a 2% pace,” remarked Simonson, a Reed webinar panelist. “I see little improvement from that slow growth, with spending recovering a little from its bleak 2% year-over-year increase last July to 5% to 10% for the year as a whole, still a good deal less than the 16% jump last year.”

Movement in sub-sectors

But the bigger, more telling story in the non-residential sector may lie in what’s happening in some of its varied components. Drilling down, if forecasts are accurate, signs of some telling shifts and trend confirmations/reversals could poke through in 2014.

Institutional construction, for one, might finally reverse course and turn up modestly after several years of decline and stagnation. There will be several drivers leading to a net gain, forecasts suggest, including a possible increase in state and local government spending that will boost expenditures on new schools and public structures; a resumption of spending on new hospitals and health care facilities to accommodate increased health care demand and access; and new amusement/recreation facilities catering to consumers with a bit more “fun” money in their pockets.

There’s broad consensus that virtually every sub-sector of institutional will either reverse course and turn up or accelerate in 2014. Dodge sees the sector up 2% to $89 billion after falling some $44 billion since 2008. The AIA consensus number for 2014 reflects a gain of better than 7% after being down 1.8% in 2013. Within that, health care could grow nearly 8% and education 7%. In addition, the AIA billings index had been up four straight months as of October.

“One change that’s expected for 2014 is that institutional building will no longer be pulling down non-residential building and total construction,” says McGraw Hill’s Murray. “News out of the state and local government sector has turned positive, and there could be more bond issues being passed for schools and other facilities. This might finally help turn the institutional building market around.”

Commercial building construction is on track for another respectable year. Growing confidence in a pickup of dormant consumer spending is spurring more investments in retail space, warehouses, and even office buildings, despite lackluster employment growth. Dodge sees new CPIP picking up 17% or so again, almost within reach of levels last seen in 2008. AIA has commercial advancing almost 12%, two percentage points better than 2013.

“A lot of the commercial growth is tied to residential construction, and there’s usually an 18- to 24-month lag on that,” says Reed Construction’s Chief Economist Bernard Markstein. “There’s still a long, hard road we have to follow here.”

After surging in 2011, only to fall back in 2012, manufacturing construction regained its footing in 2013. With fortunes heavily tied to capacity utilization, the trade outlook and confidence in long-term economic trends, the sector has been on a hair-trigger as signals become harder to reliably translate. They’re flashing a light shade of green heading into 2014, leading Dodge to conclude, with some caveats, that CPIP could tack on another 8%, to 54-million-square-feet worth $15 billion.

“With moderately healthy capacity utilization, manufacturers are likely to go ahead with investment plans should they see that uncertainty relative to political wrangling is subsiding, and U.S. economic growth is picking up,” reads the Dodge report.

The biggest shifts in non-residential construction in 2014 could be in the category’s largest and smallest, non-building, components. Dodge sees public works spending reversing course and dipping 8% to $109 billion, and electric utility construction falling for the second year in a row to $16 billion, down 33%. Uncertainty on federal discretionary spending will take a toll on public works projects, while supply-demand imbalance and changing calculations on fuel sources will impact generating projects.

Factoring in fragility, mixed signals

With those two exceptions, there are few truly downbeat forecasts for any major construction sectors in 2014. Predictions for healthy total construction gains appear to factor in the ample uncertainty that flows from a stubbornly dysfunctional political climate in Washington, D.C., and the challenges of unwinding Federal Reserve stimulus (designed to keep a lid on interest rates) that could be propping up the economy. Surprises there, and thus in calculations about the economy’s true health and trajectory, would be game changers, clearly putting a damper on new construction linked to a firming economy and growing optimism.

But flickering signs of GDP growth, consumer spending, and employment gains, stepped-up lending activity and prospects for cheaper energy as North American production escalates mean the fundamentals look at least favorable for construction in the short term. Evidence of a sustainable trend is still hard to find, though, especially in a climate where government fiscal policy seems tied in knots.

“Economic growth has been barely acceptable, and the recent government shutdown did not help, costing us about a quarter-point in fourth-quarter GDP,” said Reed’s Markstein. “We have a few more months to thrash out a budget and get rid of the debt ceiling issue, but in crafting a resolution we could see sharp cuts in government spending in the short run. We’re looking for continued slow growth, with some pickup again early in the year, but until we resolve some of these crises, we’ll have uncertainty that will hold down investment.”

{kind=link}

{kind=link}

{kind=link}

Incurable optimists, though, might be able to hang their hats on this nugget that suggests looking backward to see forward: Construction activity since the “trough” of 2011 has been closely tracking the same upward slope seen in the 1991-2011 trough-to-peak-trough cycle, Murray points out. That cycle peaked in 14 years before turning down, and started with a much more modest upturn than the prior two cycles that lasted nine and seven years, respectively (Fig. 6).

If that pattern holds, construction growth in 2014 could lead up to a pause that refreshes, followed by eight years of steady growth, before it takes another breather on its way to the peak. Murray is skeptical that another 20-year cycle is at hand, unless something like a game-changing energy revolution occurs. But he thinks 2014 will mark another step in the upward phase of a respectably long cycle.

“We’re kind of tracking the path we saw back in the early 1990s, and I’d say there’s evidence that this is a cycle, not a lost decade for construction — and that there still is a cyclical element to this industry,” says Murray.

Zind is a freelance writer based in Lee’s Summit, Mo. He can be reached at [email protected].

About the Author

Tom Zind

Freelance Writer

Zind is a freelance writer based in Lee’s Summit, Mo. He can be reached at [email protected].